Having attended another excellent Octo-Members virtual pub event Wednesday (I also enjoyed a ‘virtual’ alcohol free beer 🍺) the topic circled the old chestnut for suitability and appropriateness of centralised investment propositions (CIP) for the business and their clients.

This is a subject that has stood the test of time in generating debate over issues such as value chains, fund managers ego’s, regulatory stance of shoe-horning or retro fitting and off course the old ‘can I use one platform or investment proposition across my client base’ question…

The truth of the matter when debating and attempting to find solutions is that there is no definite solution, it all depends on variables such as the client’s on-going needs and objectives, the firm’s business model, regulatory directives such as PROD and advice suitability, technology solutions and research tools and good old trusted professional behaviour across all relevant stakeholders such as product manufacturers, fund managers and wealth managers, advisers and planners.

What is crucial is that the trusted behaviour meets the high standards the FCA set across conduct (behaviour) and competence (skills) plus ensuring the right culture is in place for individuals to ‘do the right thing’ by their clients. Integrity is key.

It was clear (to me) from the Octo-members virtual pub debate that there are many moving parts but also each component is no silver bullet. For example technology built well is an enabler to efficiency’s across communications, operations, systems and controls but on its own is not going to solely fix the CIP or advice suitability conundrum.

What’s needed is a joined up approach with suitability being the end product of the sum of many parts coming together seamlessly.

The PROD rules can help here. They are aimed at ensuring the product manufacturers build their products with the end user’s needs in mind I.e. the client. Plus, they also need to ensure such products are distributed correctly to the end user, so the Retail Investment Advice (RIA) firms research and due diligence comes in as does, wait for it…client segmentation.

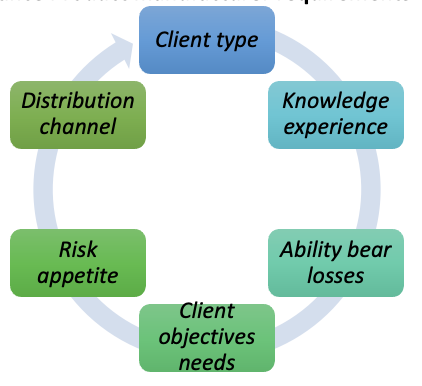

Figure 1 Product Governance Product manufacturer requirements

Figure 1 above illustrates PROD 3.2.1R. which demands:

- A manufacturer must ensure their financial instruments are designed to meet an identified target market of end clients

- Ensure the compatibility of their distribution strategy with the target market and

- Take reasonable steps to ensure distribution to the target market.

We then have the RIA advice suitability requirement and thus the need to segment client by needs and ensure the services and products meet those needs.

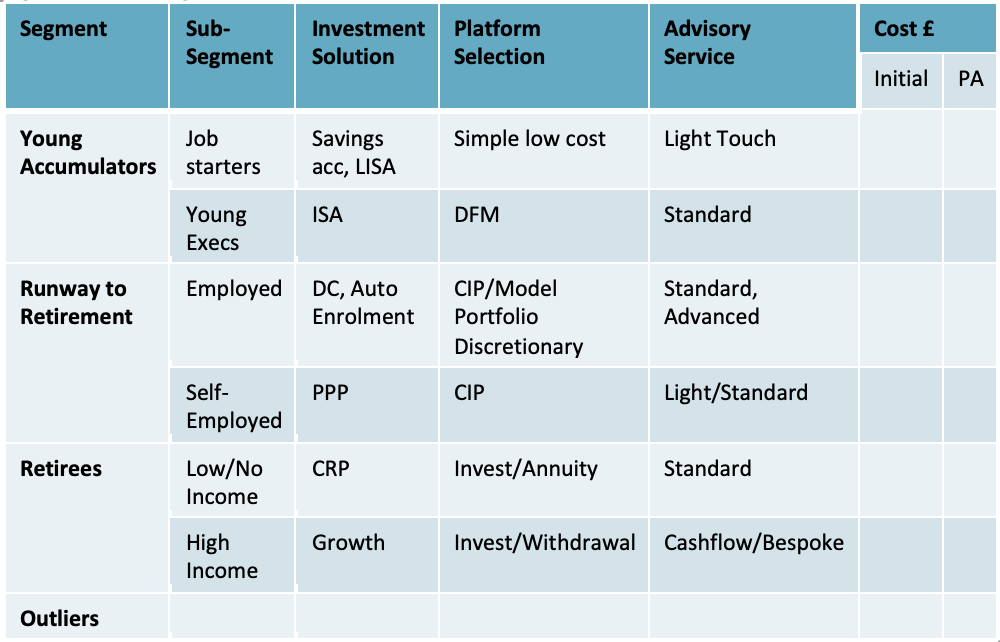

Figure 2. Client segmentation framework

*adapted from Rory Percival Consulting's segmentation table

Figure 2 illustrates how firms can map out their client’s on their financial planning journey’s and ensure services, products costs and charges are suitable for those segmented clients. This also evidences PROD 3.3.1R in action in that;

- The distributor understands the products it distributes.

- Has assessed the compatibility of the product with their client needs, taking into account the manufacturer’s target market requirements and

- Ensures products meet client best interests.

I can hear the holistic lifestyle financial planning devotees screaming (I'm with them btw and practised planning when I was active within the wealth management industry) it’s not about the product and they are quite right when it comes to the client planning journey. It’s about their goals and aspirations. So this is where technology can help across cashflow, attitude to risk and research tools. They can communicate to the client, that they are on track (or not as the case maybe) and showcase the most suitable products that will act as the ‘fuel’ to get them there. In applying emotional intelligence the RIA’s soft skills and streamlined suitability reports will ensure their clients are coached through the planning process without getting too hung up on the technical product details.

By taking a holistic approach across the client journey, regulatory framework, technology and the RIA competence, conduct and culture, we can go a long way to ensuring trusted partnership relationships with clients who know their advisers have got their best interests at heart and have the tools and technology to ensure they remain on track to meet their goals.

Please click the below icon link to MO®'s #RegTech platform and learn more about MO® today..