The FCA's latest Retail Mediation Activities Return (RMAR) provides another valuable insight into the changing shape of the UK intermediary market. Looking beyond the headline revenue figures, the 2025 data continues a trend that has become increasingly evident over recent years: there are fewer regulated firms, larger businesses are accounting for a greater proportion of market activity, and firms are operating under increasing operational and regulatory pressure.

For advisory businesses, growth is clearly still achievable. The challenge is whether firms can scale profitably when regulatory expectations, operational complexity and compliance costs continue to rise.

Revenue continues to grow despite market consolidation

The RMAR figures show strong revenue growth across all three major intermediary sectors.

Yesterday I attended the launch of the FCA'sMills Review, which is likely to become one of the defining papers shaping the future of AI within UK retail financial services. Rather than debating whether firms should adopt AI, the Review focuses on a more important question:how do we accelerate innovation while maintaining consumer trust, market integrity and effective supervision?

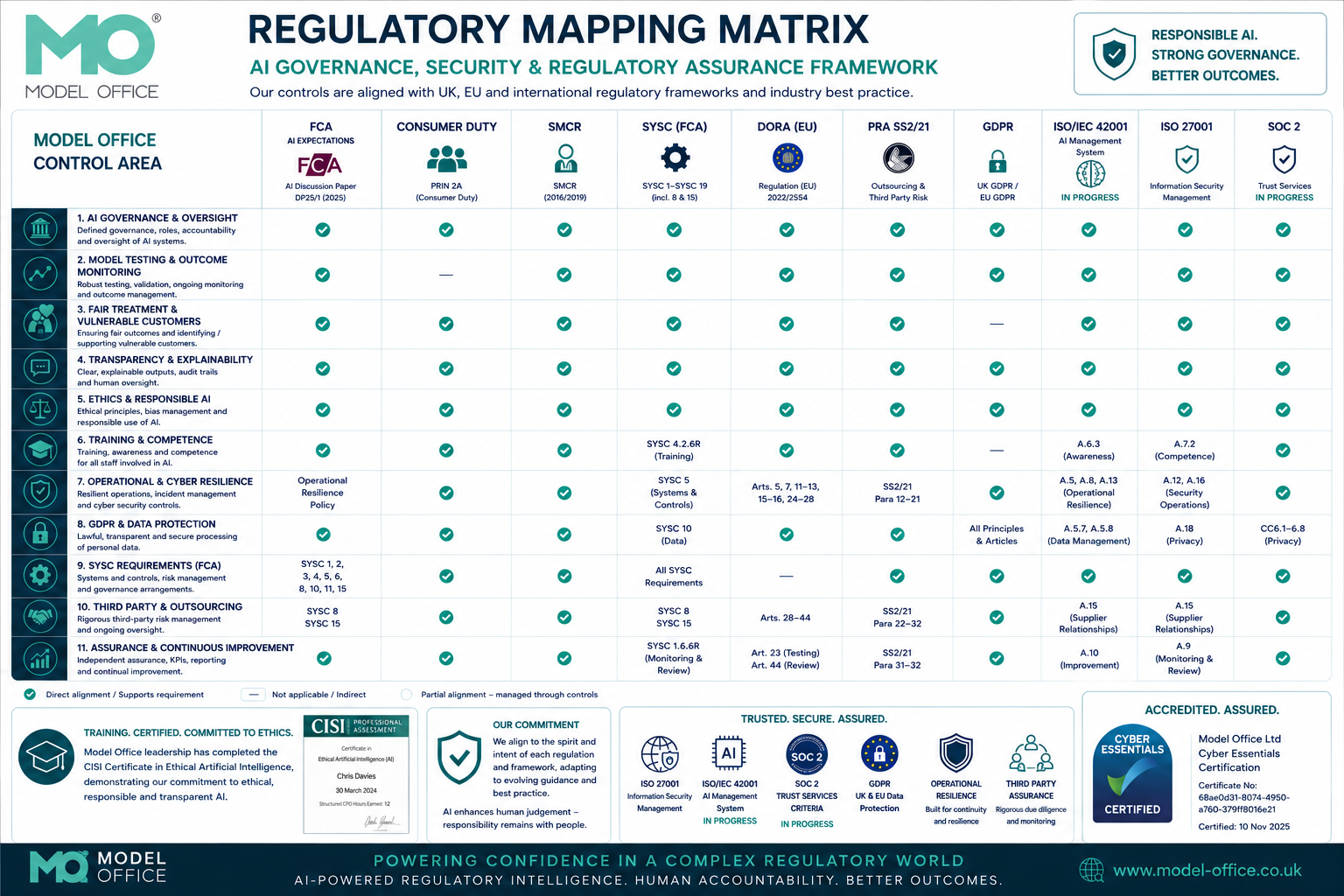

Why AI Governance Matters: Moving Beyond the AI Marketing Brochure

Artificial Intelligence is rapidly becoming embedded within financial services. From RegData analytics, client file reviews and compliance monitoring through to suitability assessments, customer support and operational oversight, firms are increasingly relying on AI to improve efficiency and decision-making.

The FCA’s recent good and poor practice review of Consumer Duty board reports is clear on one point: narrative without evidence is no longer sufficient. Boards are expected to demonstrate, with structured and reliable data, how they are monitoring outcomes, identifying risk and acting where standards fall short.

FCA SM&CR Review: More Proportionate, Still Accountable

The FCA and PRA’s latest review of the Senior Managers & Certification Regime (SM&CR) signals a clear shift in regulatory direction. The regulator is not stepping back from accountability. Instead, it is trying to reduce operational friction and administrative duplication while maintaining strong governance and individual responsibility.

The FCA’s latest consultation paper CP26/10 is another clear signal that the regulator is continuing its shift toward a more flexible, outcomes-based advice framework, underpinned by Consumer Duty and supported by smarter, data-led supervision.

For many UK financial services firms, regulation is still approached as a cost centre or operational burden. Increasingly, that is the wrong lens. Regulation is becoming a competitive differentiator, particularly in the age of data and AI.

In January ’26, Model Office were lucky enough to be selected to participate in the FCA inaugural AI Lab Supercharged Academy. Thirty two AI firms coming together with the excellent support of Centre for Technology and Entrepreneurship (CFTE) for a ten week immersive programme which has contributed to some the most important stages in the evolution of our RegTech business.

FCA review: consolidation in financial advice and wealth management – what firms need to do next

At the Consumer Duty Alliance Conference Manchester, Nick Hulme, FCA’s Head of Department for Advisers, Wealth & Pensions Supervision, highlighted that the regulator sees their 2025 advice market survey as serving a dual purpose: supporting the regulator’s supervision and policy work, while also enabling firms themselves to benchmark their business models, advice processes and outcomes against peers of a similar size and profile.