The FCA’s consultation on simplifying advice rules is a structural reset for the UK advice market. It is not a dilution of standards. It is a move toward clearer, more proportionate regulation, with Consumer Duty as the anchor.

The recent NVIDIA keynote set out a clear direction for AI. The key message is simple: the industry is moving from building models to running them continuously in real-world use.

The latest FCA review of firm’s consumer duty implementation process has highlighted key concerns across a well-used regulatory tool that of proof of value (POV). Given that evidencing fair value across the Duty’s second outcome is highly subjective this was always going to be a big challenge for adviser firms.

The FCA's 2023/2024 business plan outlines three key priorities: protecting consumers, ensuring market integrity, and promoting competition. Let's take a closer look at each of these priorities.

Artificial Intelligence (AI) has come a long way in the past few decades. Today, AI is capable of performing a wide range of tasks, from recognizing objects in images and translating languages to playing games and driving cars. However, one of the most exciting and rapidly developing areas of AI is generative AI, which aims to create new content, rather than simply analysing or recognising existing content.

This is a topic that often comes up across social media and conferences that focus on FinTech developments within retail financial services industry. There is no doubt with the fast growing digital ‘fourth revolution’, we are witnessing rapid build and deployment of tech throughout industry products and services.

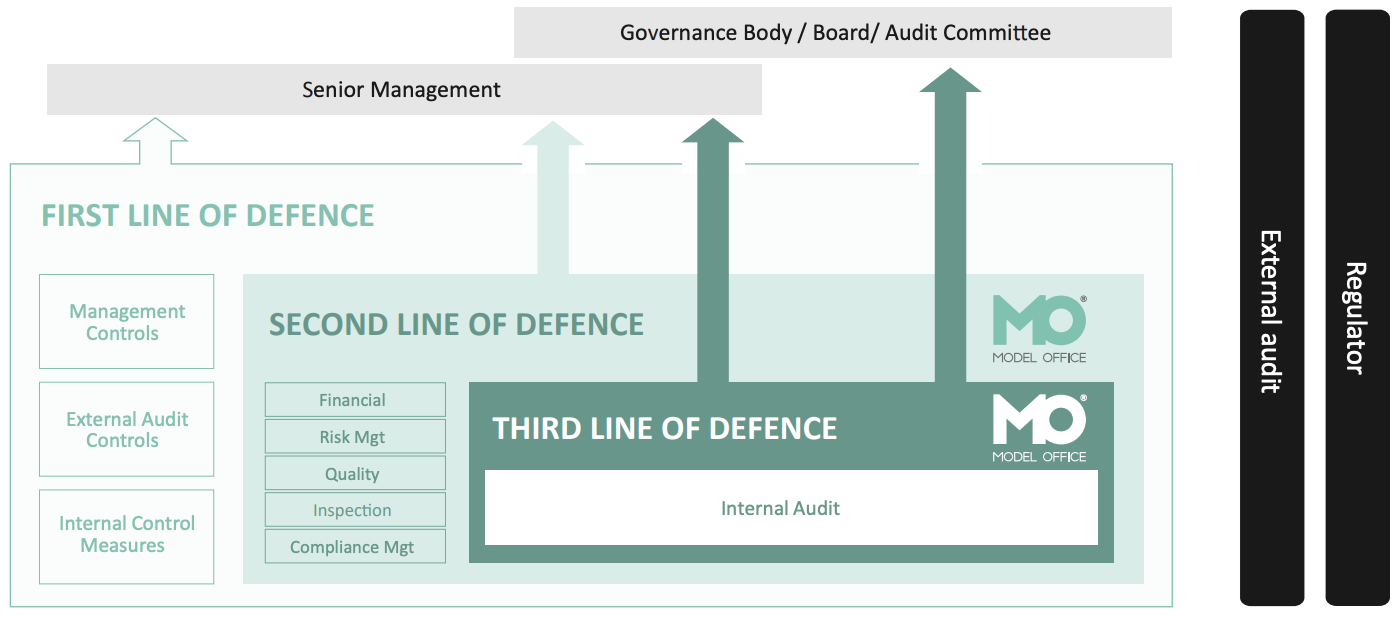

Let’s start with the top three challenges firm’s face when it comes to GRC management.

We currently have a festival of football with the UEFA European Championship, and you can be assured that each national team coach will be using data analytics to assess their own and opposition teams and players strengths, weaknesses and winning formations.

As of May 2021, RegData completely replaced Gabriel as the FCA’s platform for data collection after a lengthy roll-out to 52,000 firms and 120,000 users. Firms and their users were moved to RegData in groups, based on their reporting requirements.

The FCA first published their duty of care paper in July 2018. Two years on it is now consulting on introducing a new consumer duty. This consultation ties in with the new FCA ‘outcomes’ focused principles based framework and is open until 31st July 2021 and following section 29 of the financial service act 2021, should be introduced by 1st August 2022.